Global server market Q2 performance ‘muted’

- 10 September, 2021 15:02

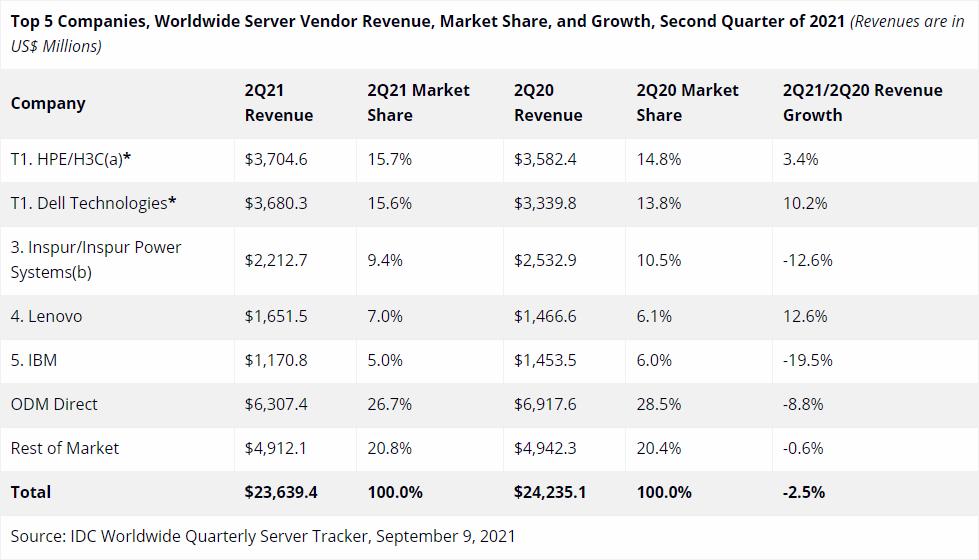

Vendor revenue from the global server market dipped during the second quarter of 2021 by 2.5 per cent, to US$23.6 billion, even despite a slight uptick in server shipments of 0.1 per cent, to 3.2 billion units.

According to research firm IDC, volume server revenue rose 5.6 per cent to nearly US$20 billion, yet midrange and high-end server revenue both declined by 30 per cent to US$2.4 billion and 32.7 per cent to US$1.3 billion, respectively.

"Broadly speaking, server market performance was muted in the second quarter as the market shifted slightly towards single socket server configurations," said Paul Maguranis, senior research analyst for IDC’s Infrastructure Platforms and Technologies team.

"While servers purchased directly from ODMs [original design manufacturer] declined year over year, some past backlog recovery within the hyperscale data centre community contributed to a large jump in this segment when compared to the first quarter of this year."

On a revenue basis, Hewlett-Packard Enterprise and H3C edged out the competition for first place during the quarter with a combined US$3.70 billion, representing growth of 3.4 per cent.

In second was Dell Technologies, with US$3.68 billion, up 10.2 per cent, followed by Inspur and Inspur Power Systems with a collective US$2.2 billion, a decline of 12.6 per cent.

IDC's analysis of the Q2 2021 server market appears weaker on a vendor revenue basis when compared to its analysis of the fourth quarter of 2020, when it claimed that vendor revenue rose by 1.5 per cent year-on-year.